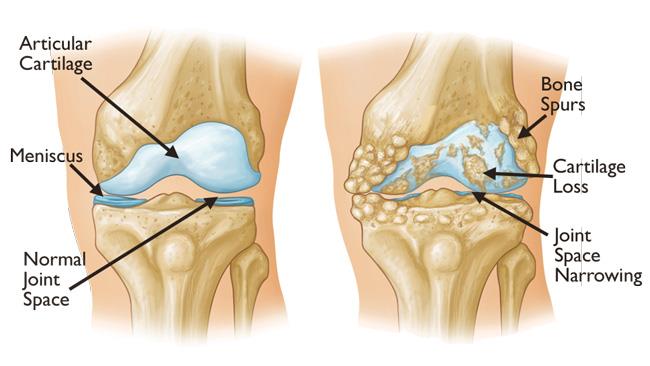

The total knee arthroplasty, also known as knee replacement surgery, involves resurfacing of the knee joint with prosthetic components to replace knee surfaces damaged by arthritis. Metallic alloys are generally used to manufacture knee implants to emulate knee movement and reduce pain. Titanium and its alloys are widely used for implants owing to their lightweight and corrosion resistance properties. Knee replacement surgery is recommended for patients suffering from severe pain and stiffness in the knee joint due to osteoarthritis or other conditions like rheumatoid arthritis. It aims to relieve pain and help regain normal knee function.

The global total knee arthroplasty market is estimated to be valued at US$ 9452.32 Mn in 2024 and is expected to exhibit a CAGR of 6.1% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights.

Market Dynamics:

Increasing prevalence of osteoarthritis is a key factor driving the growth of the total knee arthroplasty market. As per the Arthritis Foundation, osteoarthritis is the most common form of arthritis and around 32.5 million adults suffer from osteoarthritis in the US. With ageing population and rising obesity rates, the incidences of osteoarthritis are expected to increase manifold in the coming years. Moreover, development of novel knee implant designs that mimic natural knee movement better and introduction of robot-assisted knee replacement surgeries are also fueling the market growth. For instance, Stryker Corporation offers Mako SmartRobotics which allows for a precise pre-operative plan and robotic-arm assisted surgery for total knee replacement. However, high costs associated with knee replacement surgery and long recovery period involved pose a challenge to market growth.

Segment Analysis

The total knee arthroplasty market can be segmented based on type, component, and end-user. Based on type, the market is divided into fixed-bearing or unicompartmental knee arthroplasty and mobile-bearing or total knee arthroplasty. Among these, the mobile-bearing or total knee arthroplasty segment dominates as it provides better mobility and range of motion compared to fixed-bearing knee arthroplasty. Based on component, the market is classified into femoral, tibial, and patellar components. The femoral segment dominates as errors in femoral component positioning can have a significant impact on knee biomechanics. Based on end-user, the total knee arthroplasty market is segmented into hospitals, ambulatory surgical centers, and orthopedic clinics. Hospitals are the primary end-users due to availability of advanced facilities and skilled professionals.

PEST Analysis

Political: Government funding and reimbursement policies influence the adoption of total knee arthroplasty procedures. Favorable reimbursement policies are driving the market growth.

Economic: Rising healthcare expenditures and growing healthcare infrastructure are fueling the demand for total knee arthroplasty. High incidence of knee osteoarthritis due to obesity and improved economic conditions also support market growth.

Social: Increasing prevalence of knee osteoarthritis and sports injuries due to sedentary lifestyles and growing geriatric population is a key social factor. Elderly people are more prone to joint disorders.

Technological: Advances in implant materials, minimally invasive surgery techniques, and computer-assisted navigation systems are prompting greater adoption of total knee arthroplasty. Emerging 3D printing technology is also improving implant design and customization.

Key Takeaways

The Global Total Knee Arthroplasty Market Size is expected to witness high growth due to the rising prevalence of knee osteoarthritis. The global total knee arthroplasty market is estimated to be valued at US$ 9452.32 Mn in 2024 and is expected to exhibit a CAGR of 6.1% over the forecast period 2023 to 2030.

Geographically, North America is expected to continue dominating the total knee arthroplasty market over the forecast period. The dominance of North America can be attributed to factors such as growing geriatric population, rising incidence of obesity, favorable reimbursement policies, and new product approvals.

Key players operating in the total knee arthroplasty market are Depuy Synthes (Johnson & Johnson), Zimmer Biomet Holdings, Inc., MicroPort Scientific Corporation, Conformis Inc., Corin Group, Exactech Inc., DJO LLC. (Colfax Corporation), Medacta International, Smith & Nephew plc, Stryker Corporation, Baumer SA, SurgTech Inc., and Meril Life Sciences Pvt. Ltd. Depuy Synthes (Johnson & Johnson) and Zimmer Biomet Holdings, Inc. are the leading players due to their robust product portfolios and global presence.