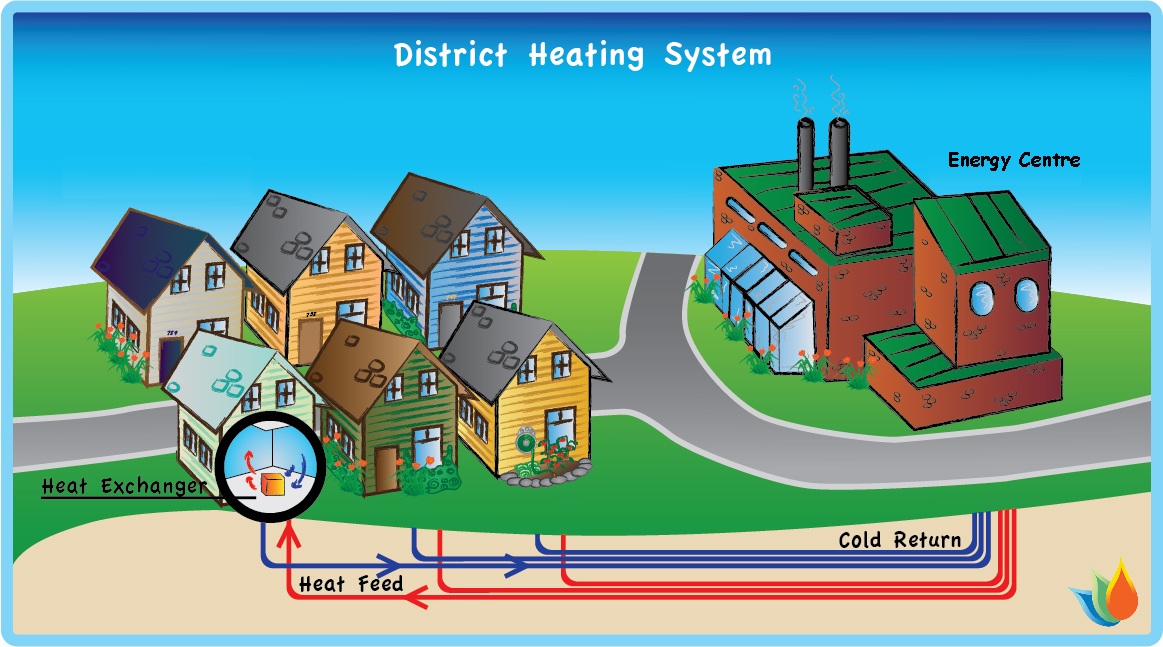

District heating systems are used for distributing heat generated in a centralized location for residential and commercial heating requirements such as space heating and water heating. District heating has advantages over individual localized heating systems as it increases energy efficiency, reduces carbon emissions, and offers competitive heating costs. The rising demand for sustainable and efficient heating solutions for residential, commercial, and industrial establishments is driving the adoption of district heating globally.

The global district heating market is estimated to be valued at US$ 50.8 billion in 2024 and is expected to exhibit a CAGR of 1.5% over the forecast period 2023 to 2030.

Key Takeaways

Key players operating in the district heating market are Vattenfall AB, SP Group, Danfoss Group, Engie, NRG Energy Inc., Statkraft AS, Logstor AS, Shinryo Corporation, Vital Energi Ltd, Göteborg Energi, Alfa Laval AB, Ramboll Group AS, Keppel Corporation Limited, and FVB Energy.

The key opportunities in the district heating market include development of low carbon heating infrastructure in developing nations, integration of renewable energy sources with district heating systems, and expansion of existing district networks to connect new residential and commercial complexes. Technological advancements such as utilization of waste heat recovery and integration of smart grid and monitoring systems with heating networks offer new growth prospects.

Market drivers

Favorable government policies and regulations promoting efficient and sustainable heating solutions is a key driver for the district heating market. Most countries in Europe have laid down policies mandating connection to district networks for new developments. Subsidies and tax rebates for adoption of renewable-based district heating further encourages its deployment. Stringent norms to reduce carbon footprint from buildings and growing focus on energy independence at national levels also stimulate the demand for district heating globally.

Current challenges in the district heating market

The district heating market is currently facing challenges such as high installation and distribution costs, aging infrastructure, and integration of renewable energy sources. Setting up new district heating pipelines requires huge capital investments and retrofitting existing pipelines to reduce heat loss is also expensive. Many countries have ageing district heating infrastructure that was set up decades ago. Replacing or refurbishing old pipes and systems increases operating expenditures. Additionally, integrating more renewable and low-carbon energy sources such as solar thermal, geothermal, biomass into district heating networks is technically challenging and increases costs.

SWOT Analysis

- Strengths: Centralized provision of heating reduces costs. District heating systems can utilize waste heat from industries and power plants. Allows integration of renewable and low-carbon energy sources.

- Weaknesses: High setup and distribution costs. Difficult to expand networks into new areas. Dependent on fossil fuel sources in some regions. Old infrastructure needs upgrades.

- Opportunities: Investments in modernization and expansion. Growing focus on energy efficiency and decarbonization presents opportunities. Integration of waste heat recovery and renewable sources.

- Threats: Cost competitiveness against individual heating systems. Disruption from distributed renewable heating solutions. Uncertainties from energy policies and regulations. Climate change impacts on heating/cooling loads.

In terms of value, the district heating market in Europe accounts for the largest share globally, estimated at over US$ 30 Bn in 2023. The high population density and cold climate of many European countries have historically supported large district heating networks in the region. Another prominent geographical region is China, where district heating finds extensive usage across Northern cities. The market in China is projected to reach a value of around US$ 8 Bn by 2024.

The fastest growing regional market for district heating is expected to be Asia Pacific excluding China and Japan. Countries such as India, Indonesia, and Thailand are witnessing rapid urbanization and infrastructure growth, which is likely to drive the development of new district heating projects catering to both residential and commercial needs. The Asia Pacific district heating market excluding China and Japan is estimated to register a CAGR of around 3% during the forecast period between 2023 and 2030.