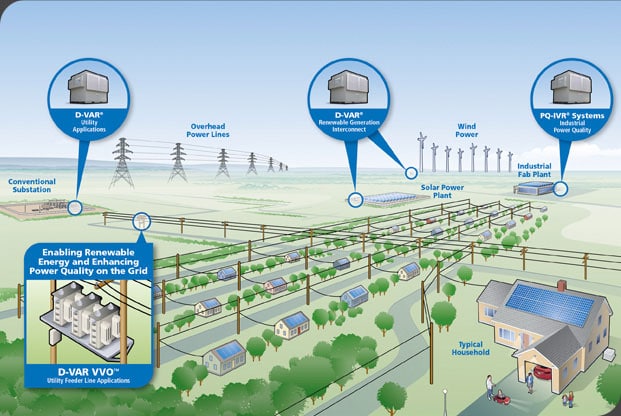

The distributed generation market involves small-scale power generation technologies that are located close to the end-users of the power. These technologies include renewable sources such as solar photovoltaic (PV), wind turbines, micro-hydroelectric, and biomass as well as diesel generators and natural gas-fired reciprocating engines. Distributed generation provides various advantages compared to centralized power generation such as reduced transmission and distribution losses, improved power quality and reliability, energy security, and self-consumption of renewable energy. The rising environmental concerns along with government initiatives and policies to promote renewable energy are driving the adoption of distributed generation systems across both residential and commercial sectors. The Global distributed generation market is estimated to be valued at US$ 364.46 Billion in 2024 and is expected to exhibit a CAGR of 14.% over the forecast period 2024 to 2031.

Key Takeaways

Key players operating in the distributed generation market are Siemens AG, General Electric (U.S.), Schneider Electric SE, Mitsubishi Motors Corporation, and Capstone, Activ Solar GmbH, Ballard Power Systems Inc., Fortis Wind Energy, GE Power & Water, Juwi Inc., Sharp Corporation, Cummins Inc. (U.S.), Caterpillar Inc. (U.S.). The increasing investments by these players in clean energy technologies will help boost market growth.

The growing emphasis on renewable energy targets by governments worldwide presents significant opportunities for distributed generation system providers. Countries across regions are formulating Net Zero emission goals which will drive the deployment of renewables in both utility-scale as well as distributed applications. Technological advancements are also improving the efficiency and reliability of renewable resources.

Advances in energy storage, power electronics, and smart grid integration are making distributed generation systems more feasible and competitive compared to traditional grid-connected systems. The adoption of lithium-ion batteries and other upcoming storage technologies can help address the intermittent nature of renewable sources and ensure dispatchable power supply. Two-way power flow capability and integration with IoT are enhancing grid flexibility and maximizing asset utilization.

Market drivers

The use of renewable energy resources for distributed power generation is a major driver for the market. Solar and wind energy are abundant, widely available renewable resources that can help reduce reliance on fossil fuels. The falling costs of these technologies along with more efficient and durable systems are making distributed renewable generation economically viable for both commercial and residential sectors. Government initiatives in the form of net metering policies, tax credits and net zero goals are also fueling market demand. The need for reliable and secure power supply especially in remote areas without grid connectivity creates opportunities for off-grid distributed solutions. The market is expected to witness significant growth over the forecast period owing to these factors.

Current challenges in Distributed Generation Market

Here are some of the current key challenges being faced by the distributed generation market:

– Interconnection issues: Connecting distributed energy resources like solar panels and small wind turbines to the existing electric grid can pose technical challenges. Utilities need to ensure the safety and reliability of grid operations.

– Policy and regulatory barriers: Lack of clear, uniform policies and regulations around topics like interconnection standards and net metering poses a major roadblock for the growth of distributed generation.

– High initial installation costs: The upfront capital costs for installing solar panels, battery storage or other distributed generation technologies can be quite high, limiting adoption rates. Incentives and financing options need strengthening.

SWOT Analysis

- Strength: Renewable sources like solar and wind are abundant and help avoid dependence on imported fuels. Distributed systems also offer enhanced energy resilience during outages.

- Weakness: Distributed generation from renewable sources suffers from intermittent availability. Energy storage solutions are still expensive.

- Opportunity: Rapid technological progress is continuously reducing costs of solar panels, batteries and other distributed generation components. This will boost affordability and uptake over time.

- Threats: Fossil fuel lobby groups aim to protect centralized utility business models. Stricter emissions regulations can impact operating costs of diesel gensets negatively.

Geographically, North America accounts for the largest share of the distributed generation market currently, in terms of value. This is mainly attributed to supportive government policies promoting renewable adoption in the US.

The Asia Pacific region is poised to become the fastest growing market for distributed generation during the forecast period. Presence of emerging economies like China and India experiencing strong economic growth and increasing demand for electricity makes the region highly promising.