3D integrated circuits (3D ICs) allow integrated circuits to be stacked vertically as well as placed side by side on the same substrate area. This vertical stacking provides advantages such as higher speeds, smaller form factor, lower power consumption, and increased functionalities. 3D ICs help reduce the length of interconnects between logic blocks, memories and buses, enabling faster communication between components. With continued miniaturization of semiconductor components, 3D ICs have emerged as a viable technology to improve performance and meet demand for compact, low-power electronic devices.

The Global 3D ICs Market Demand is estimated to be valued at US$ 19511.73 Bn in 2024 and is expected to exhibit a CAGR of 12% over the forecast period 2024 to 2031.

Key Takeaways

Key players operating in the 3D ICs market are Aquahydrex, Inc., MAN Energy Solutions, Electrochaea GmbH, ITM Power PLC, EXYTRON GmbH, Hydrogenics Corporation, Hitachi Zosen Corporation. These players are focusing on developing new 3D IC techniques and architectures to address issues related to power consumption, density, and yields.

The growing demand for portable consumer electronics such as smartphones, tablets, and wearables is driving the need for power-efficient 3D ICs. Miniaturization of these devices requires continued scaling of chip configurations, fuelling adoption of 3D IC technology.

Major electronics companies are expanding their 3D IC manufacturing and design capabilities globally. The technology is witnessing increased investment and research especially in Asia Pacific and North America region to cater to the surging demand from applications such as networking, computing and data centers.

Market Key Trends

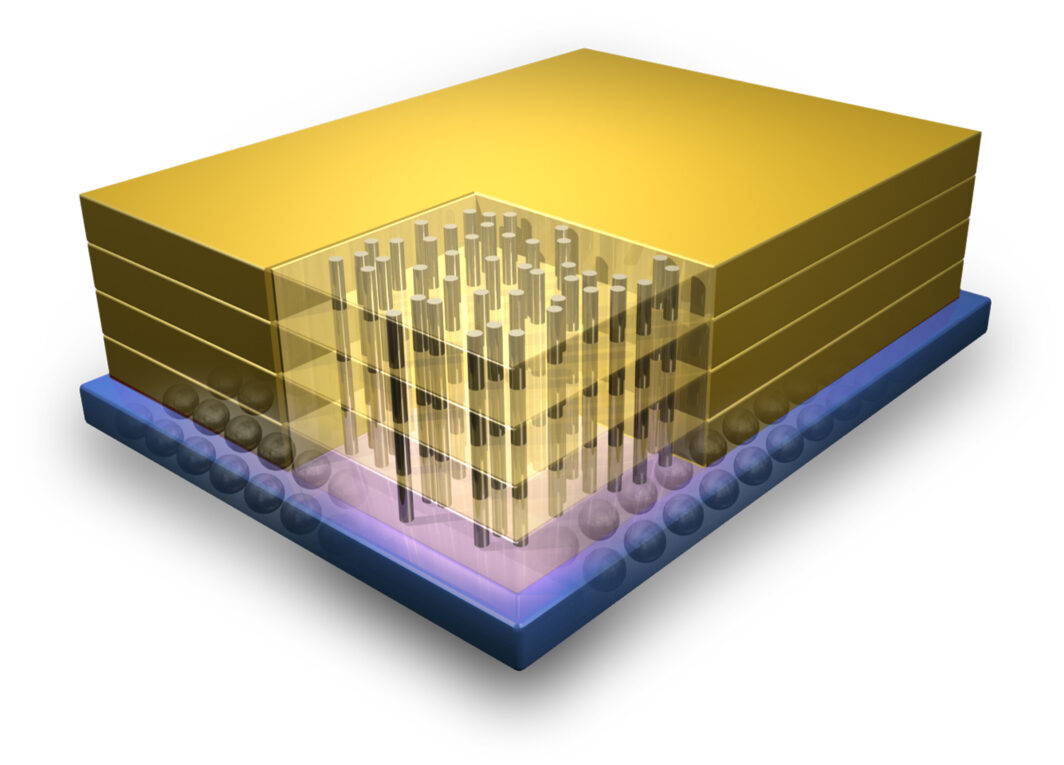

Through-silicon vias (TSVs) is a widely used 3D IC integration technique that involve creating vertical connections or vias through the silicon wafer or die. TSVs enable stacking of silicon dies and achieving high-density 3D chip packages. The trend of using TSV-based 3D ICs is growing across various applications due to advantages like improved productivity and reduced cost over alternative technologies. Emergence of new TSV fabrication techniques will continue to drive the 3D ICs market over the forecast period.

Porter’s Analysis

Threat of new entrants: High capital investments and technology requirements pose a challenge for new players. Bargaining power of buyers: Some large technology companies have significant bargaining power over suppliers. Bargaining power of suppliers: Few players dominate the technology making suppliers dependable on them. Threat of new substitutes: Emerging alternative solutions can replace 3D ICs but they are still in development stage. Competitive rivalry: Intense competition exists among major players to gain market share through technological advancements.

Geographical concentration in value terms

North America region currently accounts for the largest market share owing to heavy investments by semiconductor manufacturers and technology companies in the region. Presence of major players and government funding for R&D activities in the US and Canada further supports the growth of 3D ICs market in North America.

Fastest growing geographical region

Asia Pacific region is expected to grow at the highest rate during the forecast period due to increasing investments towards semiconductor technology development in major emerging countries like China and India. Growing demand for consumer electronics and electrical vehicles provide considerable opportunities for 3D IC vendors in Asia Pacific.

*Note:

1. Source: Coherent Market Insights, Public sources, Desk research

2. We have leveraged AI tools to mine information and compile it